As a parent with kids, I really don't know how folks are getting by with the prices of everything. I know folks who keep eating out, buying new vehicles, and even building new houses and I'm left scratching my head wondering how they afford all of this.

I'm not saving nearly as much as I was years ago and I think my "lifestyle" has decreased post COVID (few vacations, eating out is a treat, gifts are for birthdays/holidays). Is everyone swimming in debt?

There is a _LOT_ of debt being added, household debt is up to something like 17 trillion dollars from like under 10 trillion pre pandemic.

IMHO vehicles are huge drivers of debt. There are almost no cars under $30k now, and the average sale price of new cars is pushing up near $50k. This is for bog standard stuff like Hondas and Fords, not luxury cars. Used cars are incredibly expensive too. People are financing cars for well over 5 years now--I've heard of people on 6 and 7 year loans now just to make monthly payments possible. It's nuts.

> is a _LOT_ of debt being added, household debt is up to something like 17 trillion dollars

Household debt to GDP is around at a multi-decade low [1]. Payments as a fraction of disposable income, similarly low [2]. Total debt is rising [3]. But non-housing debt rose 5.8% from Q2 2022 to the same quarter '23; that's about inflation.

GDP isn't a good metric to compare household debt to. The US has an incredibly unequal society (see Gini index) and a lack of welfare compared to other Western countries. In aggregate, it means that debt is likely higher for households where that matters. The poor.

> GDP isn't a good metric to compare household debt to

It's a fantastic metric to compare aggregate debt to. It isn't the end of the story, which is why I also cited debt payments to disposable income.

American households are not, in aggregate, in a painful or even deteriorating position with respect to their debt. That doesn't mean many households, or even entire regions, e.g. West [1], aren't in pain.

Disposable income as an aggregate doesn't show a income-level class (my point). Unfortunately having up to date information on economic status given the income level is hard to get.

One reason is that in aggregate it doesn’t matter all that much: The differences between US means and medians for household financial stats are substantial but not overwhelming—and more importantly in this context, largely trend together.

It's not the technical poor that suffer the most in the US, it's the next block up, the low income working class.

The US has free healthcare for the bottom ~25%, including the poor. If you are in the low income working group, you're often largely out of luck. Those are the people suffering the most. They often don't qualify for EBT cards, they don't qualify for free healthcare, they don't qualify for housing subsidies, and so on.

The stats often don’t include benefits as income so it’s hard to really understand what’s going on.

“Free healthcare” in the form of Medicaid is a bit generous of a description for people under 65 and over 18. Few providers take it, and the benefits are really bad in many places.

How about both groups suffer far more than they should in any civilized, modern society. It’s not a contest which group is screwed over the most, let’s instead focus on why/how/what and solve.

Solid point. With inequality like it is, we really need to use metrics like median household debt and income to make any sort of meaningful conclusions.

I think the issue that this metric doesn’t measure is that there are households with debt. And there are many that don’t even keep credit card debt.

So the metric to measure “working class burden” (or whatever) is the percent increase in consumer, non-housing debt for people who had debt.

Well off people who went from $0 credit card debt to $0 while having their networth double since 2020 (high gdp) are not very useful to predict bankruptcy or political upheaval like people who went from $5k to $40k in credit card debt, are renting so didn’t see their networth go up and had their wages increase 5-10%. Those people are having a really rough time. And are worse off now day to day, and have increased exposure to risky negative events.

IMHO vehicles are the main reason Americans don't feel as rich as they actually are. I've spent the past year living in 22 countries in Europe, Asia, and South America and it's pretty clear in comparison that this is where the money is going. Americans have way, way more income than basically anyone else, but it's all going to cars and driving and the necessary infrastructure and costs associated.

No, it's going to housing. Auto expenses are trivial, but housing, especially where the jobs are, is astronomically expensive. In the expensive housing markets, contracting prices (new roof, electrical, remodels, landscaping...) are all priced far higher than other places in the country.

Housing is very much what I mean. The car-centric approach to life that the US takes dictates a very particular type of city construction and infrastructure to facilitate it. Single family homes require more land, low density housing costs quite a bit more to supply with power/water/sewage/roads. Even apartments in the US frequently feature parking and the streets for you to take your car and commute to work and back. As I said, it's quite apparent comparing the US to dozens of other countries, the amount of space dedicated to cars, huge parking garages.

Every apartment I've lived in outside the US I've been closer to at least one grocery from my front door than a parking space I'd be likely to find in a US suburban shopping center would be. A two minute walk down a cobblestone street usually. When I was in the US I tried to stay in as "walkable" places as I could and (other than in NYC* ) I still needed to hop in a car and drive 5 minutes down usually a 6 (!) lane street, wait at no less than two traffic lights at large intersections. We are talking about around $15-20 million of infrastructure involved in my trip to the grocery, plus wear and tear on my car, gas, a parking garage at my apartment compared to some trivial amount to maintain a pedestrian walkway. You don't notice it when you live in the US because it's just part of the background.

Not only are there the direct costs of the infrastructure, but the wasted space reduces available land and drives up prices significantly.

* NYC is a special case, Manhattan is essentially the only walkable place in the country (and even there it falls short of global standards), the geography and history impose unique constraints, and the city draws a lot of people for reasons that aren't generally relevant when we're talking about the housing situation globally.

> Manhattan is essentially the only walkable place in the country

This is nowhere near true. Tons of suburbs are perfectly walkable to all kinds of stores and service you could want. I've lived in 6 places in the US and only one of them was not within convenient walking distance of plenty of stores, entertainment and services (and that one was because I chose a fairly rural area at the time).

Yes you can find unwalkable places in the US but you can also find plenty of walkable places if you look for that.

How long have you lived outside the US/Canada/Australia? I’d suggest that your definition of “walkable” is skewed by global standards. I don’t mean sometimes you can leave your car at home, I mean that you have no need for a car and even most people who can afford to choose not to own one and prefer to walk, bike, or take public transportation instead.

The New York subway system is the only mass transit system in the US which could stand up to international comparison with a straight face, and NYC is still quite car focused. Sure there are some bike lanes, a few temporary street closures and 14th is closed to private cars now during the day, but still there is no large dedicated pedestrian area in New York of the kind you find in nearly all European cities.

> I’d suggest that your definition of “walkable” is skewed by global standards.

I'd say that's trending into No true Scotsman territory. If it isn't exactly like some elsewhere, it's not true walkability?

To me the definition is very simple: a home is walkable when I can get to my daily & weekly needs by walking. Enough supermarkets, restaurants, assorted shopping, entertainment, bars and plenty of services are all within walking distance.

> even most people who can afford to choose not to own one

I think this is throwing off your walkability definition. A home can be extremely walkable even when the residents own a car. Owning a car in the US is cheap and easy so even if I walk to 95+% of my needs (which I can), it's still nice to own cars for the edge cases. That

>IMHO vehicles are huge drivers of debt. There are almost no cars under $30k now, and the average sale price of new cars is pushing up near $50k. This is for bog standard stuff like Hondas and Fords, not luxury cars.

I went on toyota.com and a base level corolla is only selling for $22,795. This includes a "Delivery, Processing & Handling" charge of $1,095. If for whatever reason you think that driving a compact car is beneath you, you can have a mid sized car (toyota camary) for only $27,515.

Goooooooood luck driving off a dealer lot with a $22k Toyota! Seriously, if you can do it then good on you!

But back in the real world the on the lot availability of cars is abysmal and most makes are sold out for months of backlog. Like if you want a Toyota minivan it's something like a 2 year wait--unless you are willing to buy one on the lot with a $10k dealer markup.

Minivans are a special case that's not a good example. Minivan's have been drastically dropping in popularity (as defined by market share)for the last 20 years. Many models have been discontinued, and remaining models are being made in much lower quantity. It's basically a very niche product at this point at somewhere around 2% of all new vehicles sold.

Now there are only really 5 models of minivan left, so any small jump in purchasing, or misforecasts by a manufacturer leads to huge backlogs.

Toyota is the worst make for this, but yeah. The Corolla quote I got all inclusive was $28K and the Camry quote was $37K so I ended up going with a Tesla 3 for $34K after taxes. Much better in every way but it’s still fucking expensive, especially with insurance

In other words, it's actually available for $22k. You just get it right now. That seems... fine? I guess it sucks for the people who need a new car in the past 2 years, but given that the average age of cars on the road is around 12 years, that's a small fraction of people. It certainly doesn't support the original claim that $30k cars are the reason why people getting in debt.

I don't think you understand how new cars are sold in the US. You can't click buttons and order the car from the website, you have to work with a dealer and convince them it's worth their time to order a car for you.

I got some bad news, there is no dealership that thinks a $22k Corolla is worth their time when dozens of other buyers are willing to spend $30-40k or more for other models. The higher the price out the door generally the more money the dealership is making.

> You can't click buttons and order the car from the website, you have to work with a dealer and convince them it's worth their time to order a car for you.

I'm well aware. It's just that toyota.com is an online resource that's easy to find and and verify. Sure, dealer pricing is more "accurate", but it requires much more legwork on my part and even then it turns the whole thread into an anecdote-fest with people saying "well the dealers in my area are charging $9000 market price adjustment (or whatever) so you're wrong!" or "I called around a few dealerships and found one that gave me a $2000 discount!". Doing a quick search on reddit for "dealer markups" in the past 6 months turns up plenty of anecdotes of people being able to secure cars with no or very little dealer markups.

In 1998 I bought a used 1989 Chevy Corsica for $1,800 all-in out the door. I'll admit I don't remember how many miles it had but it never had any major problems in all the years I drove it. There was a near unlimited sea of options for ~10 year old cars for around $2,000.

In 2023, if you want a similar size 10 year old car (2013) a quick Googling suggests you'll be paying about $10,000 minimum for a car with 100-120k miles on it. Expect to pay $20,000 if you want a low'ish amount of miles (under 25k). Keep in mind this is the price on the website which you know will be more by the time you really purchase it.

Car nowadays are significantly more reliable than back in the 80s so arguable a 10 year old car back in 1989 is the equivalent of a 15+ year one now. But yeah it's still quite a bit more expensive, $2,000 is equivalent to about $5,000 now.

> But yeah it's still quite a bit more expensive, $2,000 is equivalent to about $5,000 now.

It's not quite that much. You calculated inflation off 1989 when the sale happened in 1998.

An inflation calculator puts $1,800 @ 1998 being worth $3,375 @ 2023. It's a massive difference in how much more expensive an inflation adjusted car is nowadays.

I’m seeing cars at Carmax that are ten years old with low 100K miles for around $13K. I could probably get it cheaper. But I’ve gotten four cars from Carmax over the years and the service and the buying process makes it worth the premium.

The only car we had problems with was 10 year old Jeep for my son that we had to keep taking back for various things for the first couple of months.

The manager proactively reached out to me and offered to reimburse one month payment. After those two months, we never had a problem with it.

>> If for whatever reason you think that driving a compact car is beneath you

Armchair economist-shoppers, I love them. The other day a guy told me housing in NYC was absolutely affordable. Managed to find a bedroom for rent at $2k/mo. Sure bro, let me stuff my family of four into a shared 1br apt and then have my kids share a bathroom with some random guy in the other room.

Sure, i'd do this if I was desperate...but WTF would I want to aspire to this setup if I just spent 6yrs in college and went to a top Engineering CS program. Come on.

I don't get the last part - nobody should have to put up with this.

That's part of the problem - there are still some careers where people can "make it" and mentally say "well if you'd just done what I did, you'd be fine"

I don't think that situation is fine for anyone, and we should reinforce that. It's just not ok. People stay in abusive relationships for housing, all kinds of negative shit. Nobody should be forced to live like that.

We have the materials and the money; the system is broken.

Currently trying to buy a Corolla Hybrid (base). The best out-the-door quote I got so far is $28.5k, the MSRP is $23k. So yes, you are looking at almost $30k for the most basic car.

Other brands surely have cheaper basic options, and although I might not recommend going all the way to a Stellantis/GM car, a Ford/Honda/Mazda might be available for less and still be acceptable for quality.

Ford's business is selling as many F150's as possible. Due to the way fuel efficiency regulations work in this country it makes sense for them to axe sedans from their lineup and replace them with large cars that can be classified as trucks because their more fuel efficient "trucks" can counteract the fine they would get from selling fuel inefficient F150s.

Having gone through this two years ago at the height of car unavailability, it really was take what was available. You don’t want that $50 first aid kit that comes in a canvas bag and has a few band aids in it? Too bad, you’re buying it. (I offered to sell mine to the sales person, but he wouldn’t bite.) don’t want the rails that could just be unscrewed by literally anyone at the dealership, too bad, $500. Fortunately, those were the only things we were stuck with.

When Scion was around it was supposed to be customer driven, but the sales people were the same Toyota salespeople and couldn’t help themselves. Are treacherous people drawn to (car) sales or does sales make people treacherous?

For people who checking air in tires is not a habit, nitrogen will keep them full a bit longer. A bit scammy as sold, sure, but cars are optimized for minimal maintanice these days. For the unaware, common atmospheric air is like 80% nitrogen already.

And if you buy that car today and do basic routine maintenance there's a good chance it will still be running great a decade from now.

Cars are dramatically more reliable than they used to be, so you will get more utility than you would for the same (inflation adjusted) expenditure 20 years ago.

My vehicle is 16 years old and I have no intention of replacing it any time soon.

Can you find one a dealer will actually sell you for that price? The lowest priced base models are usually only by special order, and dealers are charging thousands in markup (https://markups.org/search.html?title=toyota+corolla)

I don’t understand why this whole thread is so in the weeds about NEW cars. New cars have never been considered to be financially prudent. Hard to sympathize with someone complaining about the prices when they’re choosing a 30k+ new car over a perfectly fine used model that costs half that.

I just went to Toyota's site and mid range V6 Camry with a few options like navigation, driving assistance, etc. is over $45k sticker price. If you want a hybrid it's over $50k. For a Camry!

That's wild to see 10 year car loans. But on the other hand I also saw some high-end Cadillacs are north of $150k brand new, so some folks are really going to do anything to conspicuously consume. I can't fathom spending so much money on a massively depreciating asset.

In many cases, people getting 40 year mortgages would be better off just continuing to rent. We just bought our first home with 10% down and a 30 year note and we’re now basically paying rent to the bank.

It’s pretty nice to be able to lock in a price for 40 years. Whereas rent will typically increase a few percent each year. So after 40 years, if you’re still there, rent will be 3-5x the original amount.

Whereas mortgage payments with a fixed interest rate don’t increase so really only expenses like taxes and insurance increase over time. So after 40 years your monthly spend may be 1.5-2x.

I’m expecting that eventually there will be an interest only perpetual mortgage where the principal never decreases so banks are basically just buying secured annuities based on the real estate collateral.

Some countries have 99 leases that sort of operate like this and I thought it was strange that people would be willing to pay to purchase these leases where they never owned the property. But I guess some stability is better then none.

> There is a _LOT_ of debt being added, household debt is up to something like 17 trillion dollars from like under 10 trillion pre pandemic

Consumer debt service payments as a percent of disposable personal income - is at 5.6%. In 2016 it was around 5.5%-5.6% - despite far lower interest rates. The same figure was 5.6-6% in the 1995-2000 years.

Household debt service payments as a percent of disposable personal income - at 9-10% this year is at one of the lowest levels in 43 years. That figure was over 11% in the 1995-2000 years.

The ratio of household debt to gdp is around 0.73%. That's lower than 2011-2019 years.

US households are in fact in decent condition, despite a loud minority of people proclaiming the end of the world. The facts do not support the dire claims.

Household assets in Q1 2023: $168 trillion. Liabilities: $19.6 trillion. $149t net worth.

Household assets in Q1 2016: $106 trillion. Liabilities: $14.5 trillion. $91t net worth.

In seven years US households added $62 trillion in assets against $5.1 trillion in liabilities.

The US has gotten dramatically wealthier in the past seven years. That's how people are affording everything.

US gdp per capita is $80,000 (with ~337 million people). That's nearly France + Britain combined. There is a vast underestimation of how much income the US has and how rich the US is.

The US median household has a higher net worth than either Sweden or Germany. And the US household income and disposable income figures are typically among the highest in the world.

Is there a way to find median gdp per capita? My question with typical per capita is that won’t reflect if all of that gain went to top 1% or the middle class.

I don’t know if there’s a good median equivalent of gdp per person as it’s not really household income.

Just moved to the Netherlands and being car-free covers something like half the rent alone. Nevermind that I don't have to deal with taking it to the shop, to get smogged, paperwork for reg and tax and insurance, etc. etc.

This can be a misleading statistic. A lot of people use credit cards as a substitute for cash, and pay off the balance every month. This is accounted as "debt" but in a practical sense it is not.

Me, I use the credit card as a 6 week interest-free loan, plus getting the cash back discount.

> This can be a misleading statistic. A lot of people use credit cards as a substitute for cash, and pay off the balance every month. This is accounted as "debt" but in a practical sense it is not.

Indeed, this is annoying nonsensical. They should not count credit card balance as debt until it has rolled over at least one payment cycle.

Every summer my credit score drops ~40-50 points when I put the upcoming school year payment on the credit card (they give a nice-enough discount for prepaying) and then a month later bounces right back up after I pay it.

I thought the Fed only counted the carried balance. So folks who pay in full every month are not counted. I did a quick search but couldn't find anything definitive.

I was able to find it by going from the cnet article to to the Fed's press release, then to the report, then the 'downloads' button, then the PDF[0]. in it:

> Credit utilization rates (for revolving accounts). Computed as proportion of available credit in use (outstanding balance divided by credit limit), and for reasons discussed above are likely to overestimate actual credit utilization.

I would expect that they are only able to see the current balance.

For me, I charge and pay every month so never pay interest. But my credit report always shows a 2-5k balance (or whatever I charged).

Theoretically, if I paid off the balance BEFORE my statement period ends it would show $0, but I never do this because I have 25 days of 0% interest to pay, so I do.

I don’t think credit reports track interest paid but that would be one way to track if it’s “real” credit card debt or people just cycling.

But also you could look at average. I average $3k over the past 10-30 years or whatever. If this increased to some new stable level it would mean an increase in income. But if it increased at some rate or increased sporadically then it means I’m taking on more debt.

So I expect if credit card debt increases in total it probably means more debt and not more people paying their balance in full each month.

Occasionally the CC company will send me an offer of a loan for very low interest for a year. I run the numbers, and if it looks good, I'll take the loan and invest the money, and pay it back at the end of the term.

The CC company, of course, is hoping I'll miss payments so they can charge me 30% interest. I disappoint them.

Being aware of the time value of money is essential for managing your finances in your own best interest.

> Occasionally the CC company will send me an offer of a loan for very low interest for a year. I run the numbers, and if it looks good, I'll take the loan and invest the money, and pay it back at the end of the term.

How do you keep that from negatively impacting your credit rating?

I’m not OP, but it I do this. Sometimes it negatively impacts a little but it’s worth it (800 vs 795 doesn’t matter too much) but usually it’s a wash because it’s $5 down in one account and $5k more in another.

But when you have $100k of available balance and $10k of debt, the credit bureaus don’t change much when you have $100k of available balance and $20k of debt for 15 months (or whatever the term is).

Now you can easily get 5% returns in money market accounts so if you take a 0% loan with a 3 percent transfer fee on $10k you can basically get $200 for “free” for the juggling. You have to determine if it’s worth it, but if you have larger amounts maybe it’s $500-2k for effectively setting some reminders and not screwing up.

Even if the amounts aren't that large, it's good practice.

I once read an article on how Amazon made money selling items at wholesale prices. The answer is astute money management. When you bought an item, Amazon charges your credit card immediately, and they get the funds right away. Amazon does not pay the vendor, however, until 90 days have elapsed.

This means they have the use of the money for 90 days, and (of course) they invest the money. Multiply this over millions of purchases, and you're making a boatload of moolah.

I do the same thing, it's just on a very small scale. It's called working the float.

Banks do it, too. Ever notice that when you get a cashier's check, your account is debited immediately? But if you deposit a cashier's check, you have to wait a day or two for the credit. The bank is doing the same thing.

Of course, banks make a lot of money on pennies because of scale. None of this is new.

I do agree that being your own bank is really smart, that's why I like DeFi so much... it makes it super easy, without any impact on your credit score.

That said, doing it at a small scale doesn't really seem like it is worth the hassle. $200 isn't worth the time or dings on your credit score. When I've done it before, other cards notice and also start to cancel you or lower your available credit as well.

I have "excellent" credit (780+), a fairly large credit line across several cards (~$100k+) and I never get those year long offers for 0% (or anything less than current interest rates) any more. Those dried up years ago. I don't see how anyone is making this work.

> How do you keep that from negatively impacting your credit rating?

It has, my credit score isn't the greatest. But I don't care. I don't take out loans to buy things because of the high interest rates. Instead, I pay for things with investments.

Borrowing money to buy things is a trap. Borrowing money to buy a new car is financially inept. Buy a beater for cash, invest what you would have spent towards a new car, and eventually the growth in that investment will provide enough to buy that new car. You'll be much better off.

I don't know how most people are doing it. For me it's because the asset bubble has inflated my stock income. I suspect a lot of folks who owned homes, stocks and other assets are feeling the wealth effect. For the rest of society, I don't know why they're not in the streets with pitchforks.

"It is well enough that people of the nation do not understand our banking and monetary system, for if they did, I believe there would be a revolution before tomorrow morning."

You misunderstand the scope of formal fallacies, which only apply to formal arguments. Most arguments aren't formal arguments, and that's ok; they aren't supposed to be. Instead of proving a conclusion from a set of premises, they rely on heuristics to draw probabilistic inferences.

In the context of a formal argument, the act of quoting Henry Ford would have been either the fallacy of appeal to authority (if the quote's provenance were meant to demonstrate its veracity), or the fallacy of bare assertion (if it were meant to stand on its own). I didn't invoke those fallacies because I understand that, outside the context of a formal argument, appeal to authority is a reasonable heuristic, rather than a fallacy. There's nothing fallacious about saying, for example: "Most doctors recommend getting vaccinated, so you should probably get vaccinated."

In this context, my reply is also not fallacious: it's reasonable to doubt the reasoning ability of a vicious anti-Semite, particularly on the subject of nefarious bankers, which is closely intertwined with anti-Semitic conspiracy theories.

The "formal" in "formal argument" does not mean "the opposite of casual". Rather, it refers to arguments which take a particular form: those that assume a set of premises, and use formal logical tools to prove a conclusion from those premises. To accuse an argument of containing a formal fallacy means: the tools you tried to use to prove that conclusion from those premises is defective, and you have not actually proven the conclusion.

However, proving a conclusion is only one possible thing that an argument may set out to do. Oftentimes, we are more interested in probabilistic evidence than in absolute proof. Thus, an argument which does not prove anything (and which would thus be fallacious if treated as a formal argument) can nonetheless be useful.

> My investment portfolio profits (or RSU vests or bonuses) never make their way to my checking account

That's your choice[1]. Some people sell upon vesting, and others liquidate periodically or to make down payments on property or health emergencies instead of going into debt. I suppose if one had a rainy day fund and the value of their RSUs doubled over one year, they may be tempted to spend the emergency fund since their net worth has gone up.

That said, I suspect you holding onto RSUs means you end up not saving as much for an emergency from your checking account, so you get an extra bit of liquidity.

1. I held onto RSUs too until I realized its indistinguishable from being paid extra cash and choosing to buy shares in my employer. I prefer rebalancing my portfolio with my preferred diversification mix.

Living through dot-bomb made me very conservative about holding options/RSUs. I won't say I haven't held them at all (and more recent history I'd have been better holding more) but in general better to take the cash.

I definitely never kept my RSUs after they vested. I always diversified them over the six months. I wouldn’t have used 25-30% of my cash income to invest in my company stock. Why would I keep my RSUs instead of selling them?

While I could live off of my base income working remotely in the burbs of Atlanta, there is no way that my friend who had to relocate to Seattle and had two kids and a wife could have managed on the same $160K base.

I always sell my RSUs as soon as I can, but the proceeds never touch my checking or savings account. I directly purchase ETFs.

When my base salary was $150k in SF, I worked a side contracting job to cover lifestyle costs so I could max out ESPP and 401k. Certainly if you have a family, you may not have the time to do that.

I promised myself since I got (re)married in 2012 that I would never work two jobs. Whatever I couldn’t do with one job, wouldn’t get done.

The reason I’m not at Amazon is for the same reason. I don’t work more than 40 hours a week on a normal basis and that’s what my new manager wanted me to do to show “improvement”.

Don’t cry for me. I saw it coming two months ago and I already had a few feelers out and I am 99% sure that one will come through within the next two weeks ago.

As you probably know, working multiple jobs doesn't mean you have to work more than 40 hours per week.

There are a many jobs that only require 20-30 hours per week. You can still limit yourself to 40 hours per week of work, but enjoy the benefits and security of multiple jobs.

Your investment portfolio profits will make it into your checking account at some point right? Otherwise why bother? Maybe this person has reached that point.

If I lost my job, then I would definitely use the money for my living costs. Until then, I prefer any bonuses, RSUs, Dividends, and interest stay in my investment account for further compounding.

I see articles like that every one to three months for the last 10 years.

I remember in 2010 there was an investigation reporting about how how shocking amount of credit card debt Americans have or etc.

I’m sure there is basis in reality, but I think these “X-type of person is having financial issues” blog articles are popular because people identifying with that problem (as small of a number of people that maybe) love sharing and pointing to the article to justify their own troubles. This creates more ad revenue for the producer.

My paycheck is quite small due to the massive tax withholding I need to pay the taxes on my RSUs. I don't currently spend more than a fraction of my shares but I certainly use some of the proceeds to pay monthly expenses. I also sell company stock as soon as I get it and diversify(currently just buying T-Bills) because keeping all your eggs in one basket(i.e. keeping your wealth in the stock of the company that pays your salary) is bad risk management.

When I was at Amazon (ie until last Friday). We had three options - sell all, sell enough to cover taxes, or sell none of it and pay taxes - some other kind of way that I never looked into.

Even if that’s not the case, what’s stopping you from selling enough stock yourself once they vest and make quarterly payments?

My tax rate was 22%+7.3% FICA near the end when I moved to Florida - a state with no state income tax.

>43% of Ohio voters voted against their own interest last week. Majority of them are in lower side of the income.

What makes you think that raising the minimum wage would be in their interest? A comprehensive study[1] that factored in hours worked found that even though average hourly wage increased, hours worked went down, so total pay actually went down.

Since that study, pretty much all blue states had significant increase in minimum wage. Even in red states, the minimum wage has gone up and yet unemployment is historically low.

1. If you don't see any problem with this line of reasoning, I invite you to look at the unemployment rate after the Fair Minimum Wage Act of 2007 was passed.

2. Looking at "unemployment" is what the study was specifically trying to avoid, because you could cut someone's hours but keep them on payroll. If you only looked at unemployment figures and average hourly wages, you might conclude that raising the minimum wage was an unalloyed good. However, if you drilled down to hours worked you'd see that they were taking home less per week.

"lower side of income" means they are roughly linked to minimum wage. For instance, when I worked at a gas station as a kid, I explicitly got a wage $1 more per hour than minimum wage. Even if it's not so explicitly linked, the implicit link is there on all low end hourly jobs. If a wage goes from significantly above minimum wage to just barely above minimum wage due to a minimum wage change and the employer doesn't raise to match, they are going to have retention and recruitment troubles.

Same. I make decent money and used to save thousands per month. Now I'm lucky to stash away high hundreds a month, but any expense like new brakes wipes that out.

I wonder how in the world everyone else is getting by. Maybe we're all just smiling and pretending here...

Without going into deep details and a budget... everything has gotten more expensive. Groceries are at least double what they were, over $1000 a month. Summer electric bill is over $300. Internet is now $140 a month. Health insurance is now over $500 per month, and that doesn't even cover the out of pocket stuff I have to pay with the kid's various visits. All streaming services have increased in price. And so on and so on.

I could go on and on, I'm sure I sound like a 'back in my day' old man. But the 'my day' in this case was just 5 years ago...

I don't understand how it's possible to go from thousands a month in savings to almost none. That's at a minimum an extra 24k in spending. Sure prices have gone up but not that much

Some comparisons. My electricity (large SFH with 2 people) is 35$ a month (11c kWh)(in Seattle I let the 2nd floor get hot and only turn on AC from like 4-7pm, and most appliances are fairly energy efficient. So I’m not sure how to spend more electricity without an EV). My internet is maybe 70$ for 1gb (which I’ve never maxed out and could lower to like 300mb if needed) for Xfinity.

Seattle is one of the most temperate regions in the USA. Outside of Alaska I doubt there's significantly lower AC use anywhere in the USA.

A quick Google search shows ~60% of households in Washington state don't even own an air conditioner. Compare that to nearly every home in the south, Atlantic states, and Midwest where AC is near universal.

Another thing to keep in mind, my utility company says my household is in the bottom 15 percent of comparable houses! So just because it’s temperate doesn’t mean individual choice can’t make a difference :)

That sounds like a you problem. I spend $400/month and that would be a lot lower without an obsessive cycling habit which necessitates eating about double the calories of a more sedentary individual my size.

Like please share a receipt that shows how you spent $325 for one week's groceries. $43/day?? Maybe you're eating fresh fish every meal?

As many other have pointed out, that seems bonkers. We’ve spent $1,128 in the past 30 days for 6 people and that includes back-to-school supplies, some sports equipment for fall sports. We buy mostly organic fruits and vegetables, milk, beef, and chicken and have a meat protein in every meal. Even that seems absurd. We use Costco for everything we can, a weekly trip to Walmart to fill out the smaller things, and Sprouts for veggies and fruit.

If you’re paying that much for groceries, one trip to Costco or Sam’s Club will probably pay for the membership.

I spend about $2,200 on a family of 4 and I really don't budget or plan meals very well at all so I think this is probably a choices thing on your part. If I did it properly I could probably get away with $1,500 a month. Not a critique though, if you have the money and that's what you want to spend, more power to you.

Inflation’s bad but it hasn’t gotten _that bad_ yet. If you’re spending $1300 per month for groceries for _one_ person you’re surely getting high end, organic everything.

We spend less than that for a 4-person household in San Francisco. We buy at Costco, Whole Foods, Trader Joe's, and the Asian markets. I think meat and fruit are our biggest expenses. If we only ate eggs and vegetables, spending would be much lower.

That's for one adult eating 3 meals at home, 2 eating 2 meals at home, and 1 eating 1 meal at home.

Groceries? That seems insane. I rarely eat out when I'm not traveling and I would be surprised if I spent a third that when I was home and don't especially go for cheap food.

401K early withdrawals are up almost 40% YoY and credit card debt is also up massively. If interest rate increases do lead to eventual job losses things will get ugly fast

real estate is the thing to watch, if even a small number job losses happen people will have no choice but to sell even if they want to keep their low interest rate(home prices have stayed relatively flat because everybody is staying put, so low inventory on paper). Interest rate increases have resulted in significantly lower buying power, so home prices will have to drop. Forced sales will cause others to rush for the exit and cause even further price drops

> I know folks who keep eating out, buying new vehicles, and even building new houses and I'm left scratching my head wondering how they afford all of this.

You can never judge people's financial situations from their spending habits.

Someone in my extended family spent years living large, buying new cars, building new houses, and wearing nice clothes. They had a family business and always said that the business wad doing well. Several years later the husband died unexpectedly. His wife was suddenly struggling to make ends meet, despite nothing actually changing with their "business".

As we later discovered, they were experts at amassing debt. The business wasn't really successful but they had used every possible angle to get more lines of credit, debt, "investments", and loans. They had even made a habit of "buying" supplies from vendors with Net 30 terms, reselling them, and then never paying the vendors back. They moved from state to state to scam new vendors every time they were blacklisted by the all of their local vendors.

That's an extreme example, but it highlights how appearances can differ so much from reality. More commonly, I think a lot of people just never learned how to save anything at all. I know an alarming number of people in their 30s who still haven't bothered saving anything more than the $1-10K they have in their checking account at a given time. When the number goes up, they spend it back down. You could have the same net income as these people but never achieve their level of lifestyle spending because you're doing some savings.

On the other end of the spectrum, many people are actually doing well. Wages are up (contrary to what you see on social media) and people's investments have done very well in recent years. Many of my friends are doing quite well for themselves by simply getting working a little harder to get jobs that pay a little above average and then carefully budgeting and investing over the long haul. Do this for a couple decades with some careful attention paid to where you live and the job you get and it's not hard to get a rather comfortable financial position by 40, especially in tech.

It's death by a thousand cuts. New backpack for the oldest, new shoes for the youngest, oil change for the wife's car, leaf guards for the gutters so they don't clog the French drain I had to have installed due to my living room flooding. Dog has to get shots or heartworm meds... Choose the month and there is guaranteed to be $250 - $2000 in incidentals as a homeowner with kids. Wife's student loans kick in next month, $750 a month. It's crippling and I am lucky enough to do fairly well financially. I'm complaining but I'm aware that millions have it way worse than I do.

> As a parent with kids, I really don't know how folks are getting by with the prices of everything. I know folks who keep eating out, buying new vehicles, and even building new houses and I'm left scratching my head wondering how they afford all of this.

I hear you perfectly. What I did a while ago was to fully embrace a more frugal lifestyle where attention and time are the most valued. So consumption went to a minimum and all that. Now after prices jumped up we’re where we started and despite being frugal we’re left with a lot less. It is quite unsettling to be honest…

I think a lot of people get into a mindset that a 25 year mortgage is meant to be paid off in 25 years, so that mindset guides their entire frame of reference for how large a lifestyle to adopt. I’m not saying to rush through a mortgage. Do whatever you want. But consider not getting into a situation where you’re somehow struggling even though you’re one of the lucky few who can afford to even own a home.

When times get tough they’re no more secure than those who make less.

I’ve seen this with many peers who have Teslas and 1.5M homes who are now struggling despite such an income.

Paying off your mortgage with an interest rate less than inflation is a mathematically verifiable horrible idea. You're short the dollar deeply. Keep that short position for as long as you can because on a long enough horizon you'll be right so long as the Fed continues to manipulate the market.

That doesn't necessarily mean lever up. But it does mean take that extra X% you'd put into your mortgage and place it in some CDs/Bonds/whatever. Or even better, if inflation is still higher than the current rate you could even use it to buy an investment property and then pay that off as slow as possible as well. Let the banks hang themselves being long the dollar!

Debt is only bad when you're losing. The problem is it takes a level of sophistication to understand when you're winning. Hence, the need for Ramsey-type all-or-nothing solutions.

I agree that people generally seem to lack a decent intuitive understanding of risk. They only look at the current state of affairs, and the upside of the bell curve. They don't seem to remember or factor in the likely potential negative side of those distributions and adjust their planning for better resilience.

> Paying off your mortgage with an interest rate less than inflation is a mathematically verifiable horrible idea.

This is often the case, but not always. It also doesn't account for the much better sleep I get at night, or the unshackled feeling I experience knowing I am debt free. There's an enormous psychological benefit that is not easily quantified.

Paying off your mortgage early only really makes sense when you're getting close enough to retirement that you need to move more of your money to less risky investments with a lower rate of return.

My point isn’t that you need to race to pay it off. But that people think “how big a home/lifestyle can I afford with this income? I’ll do that.”

You could do half that, make minimum payments if you want, and invest the rest. But either way, you find yourself in such immense control. You could lose half your income and not change your lifestyle. Or retire early. Or take bigger risks.

I’ve always been fascinated how people decide what kind of home and car and such they go for. It usually seems to be: as big as I can go. And then you’re not really that more secure. I guess you can sell your home and find something smaller, but that’s hard to do at any time with kids in school, let alone during bad times.

For sure. Being house poor is definitely a thing. My wife and I made the decision that we'd only take on as many expenses as we could afford on only one of our salaries. That's a lot easier to do when I'm an engineer and she's a doctor, but I know plenty of friends in similar situations who are still leveraged to the hilt.

It kind of depends on your mortgage rate. If your rate is low it technically makes more sense to invest your money, as that'll have a great return. If your mortgage rate is high, you might be better off paying extra each month against the principle as it'll drastically reduce how much you pay in interest over the course of the loan.

> I really don't know how folks are getting by with the prices of everything

There is a lot of regional variation in production [1] and income [2][3]. On the whole, real disposable income and savings rates are up [4].

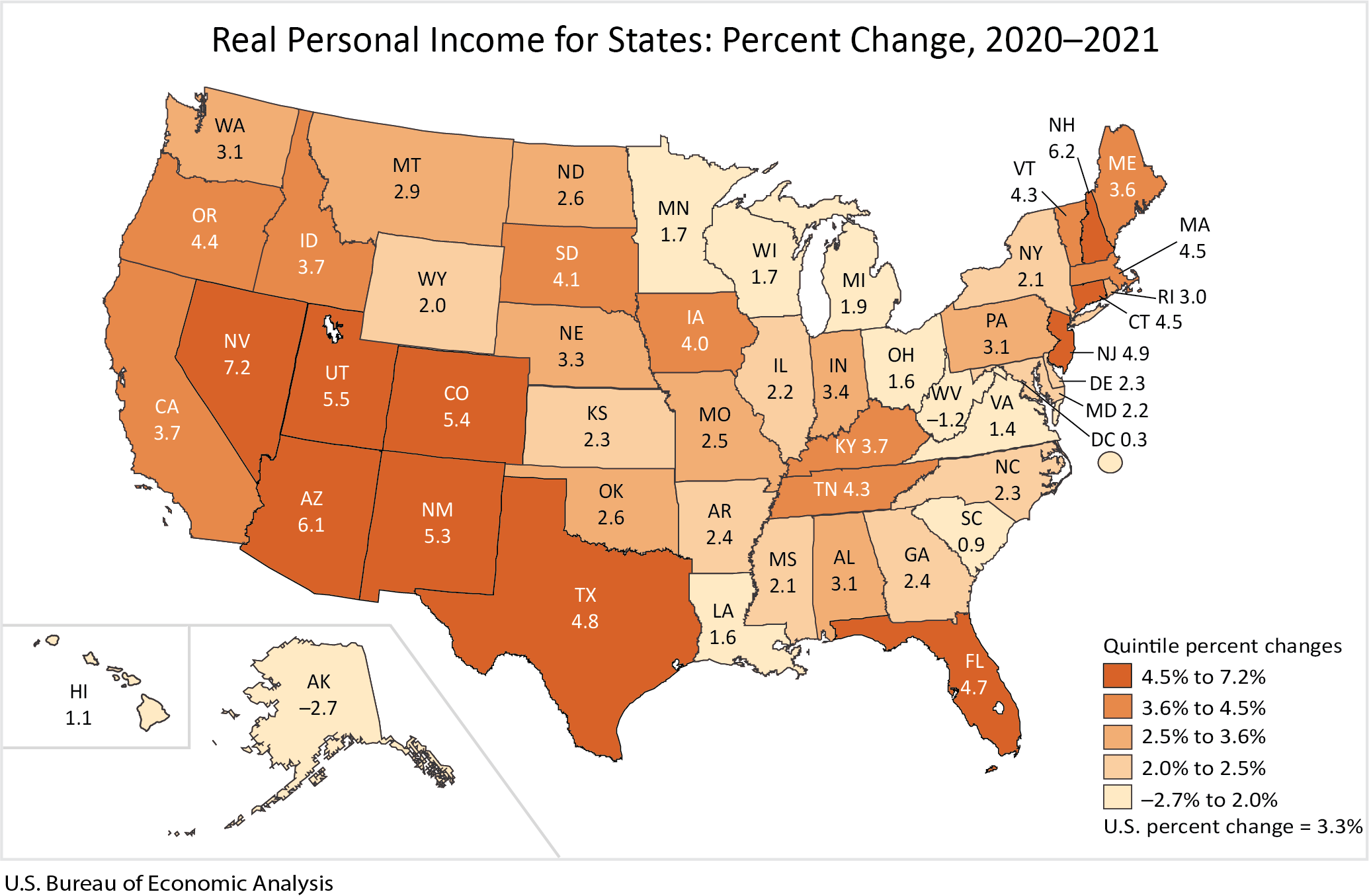

But someone in the midwest (income up, annualized, 7 to 11% Q4 '22 to Q1 '23) or Florida (7.9%) is seeing a very different economic landscape than someone in California (0.7%) or Indiana (-1%) [5].

With kid moving up to public school from pre-k we'll be saving an extra 2500$/month now. And in a couple years when our younger one is old enough that'll be another 2500$/month saved so I'm feeling pretty optimistic.

Now that is an insane price. I don’t think it even pencils out assuming the daycare is following minimum teacher student ratios and minimum wage, which means there is under the table pay going on or corners being cut somewhere.

It's a home daycare. She has 5 kids that she watches, and only one infant. I think that might be the maximum she's allowed - certainly only one infant. The infant price is more expensive as well.

Keep in mind that daycare centers themselves need to profit, so going "direct" would be cheaper.

Yes, so that is a different product than the previous poster’s $2.5k per month daycare. If workers are hard to find in your rural area, a comparable daycare might not be too far from $2.5k per month.

We looked at a (YMCA) daycare center and it was more expensive, but certainly not as expensive as that. The infant section in particular was...dystopian, though.

Also, no windows. They built it in an old mall. I couldn't get past those two things.

SAME! I barely saved this year so far and I haven’t been splurging on anything. The car I bought before the inflation burst is now 25% more now. I make good money relatively but I still feel like we’re drowning. Every grocery run is over $200 even if don’t get meat, just the fruits alone are eye watering nowadays.

I switched from regular grocery stores to aldi/lidl/walmart. And from eating out 2-4 times a month to eating out 1-2 times.

I also switched to more staple foods like lentils and beans and rice and canned vegetables instead of fresh vegetables. And to buying ground beef on sale and freezing.

It seems kind of crazy that prices keep going up and even simple “luxuries” like a coffee while networking went from $3.5 for a small latte at my local coffee shop in 2019 is now $5.5.

I think for some people it doesn’t seem to affect them and they just pay the higher prices but base costs seem to have really gone up a lot for my family. Fortunately some big expenses are fixed (mortgage and transport) but if they had to change it would be extra rough.

Because their pay also increased. People can generally afford higher prices. Real wages have remained remarkably stable in the last few years.

The article itself says this. Somehow, it manages to spin it into bad news.

>Even though prices have soared, real earnings, which adjust for inflation, are stuck at late 2019 levels.

People can afford the same lifestyles they could a few years ago. The US weathered the outbreak of war in Europe and the worst pandemic in generations without serious economic hardship. Somehow, in CNN's view, this is a problem. Real wages haven't been stable. They haven't been resilient. No, they've been "stuck".

Debt is a socialized hallucination. If people refuse to give up on it, we can just take the money back from the rich too through taxes. Reaganomics legalized looting pensions to invest on Wall Street. There's precedent for expropriation of wealth of the dying. What are a bunch of retirees going to do? Fight back against 20-30 somethings?

Boomers benefited from New Deal then killed it. There is no market, just a legalized generational Ponzi scheme.

I think the concept of cost of living areas is out the window. Mortgage and rent may be relatively COL dependent (kinda, but everyone is incentived to even it out nationwide), but for everything else I actually think the competition within big cities/"HCOL areas" drives down prices. In my "LCOL" flyover area I'm seeing $30+ pizza and $18 burgers, along with $10 beers at bars. It's insane.

I live in a—4th tier is selling it short, but 3rd tier seems generous, call it 3.5th tier—city, and am always shocked at how much cheaper good restaurant food, baked goods, et c. are in "real" cities compared to here. Anything non-shit is basically 20-50% more expensive here than in HCOL cities. Makes no sense, these places should have like 1/5 the rent costs and lower labor costs than the major coastal cities, yet, prices are sky-high and quality's often not even that good.

Groceries are about the same price. More expensive for some things, cheaper for others.

Health care's more expensive here, with lower quality, because it's a flyover red state.

HCOL only seems to apply to housing. Everything else is about the same or cheaper in "HCOL" cities. May not hold for other smaller/poorer cities, but very much does for ours.

> In my "LCOL" flyover area I'm seeing $30+ pizza and $18 burgers, along with $10 beers at bars. It's insane.

"$30+ pizza and $18 burgers" doesn't say much when you consider that there's a huge price/quality range between basic and premium offerings. For instance, a $18 waygu beef burger at a gastro pub doesn't seem very out of place at all, but a $18 mcdonalds burger would be outrageously expensive.

That matches my experience. Of places I've spent significant time in the past year, the one with the most reasonably priced food for eating out is NYC, of all places. It has very expensive places too, of course, but a lot more sub-$10 options than anywhere else I've been recently. There are even a few 99-cent pizza slice places still in business (not as many as 10 years ago, but they exist, and $2-3/slice places are abundant).

I have been listening to plenty of "finance gurus" (i.e. my favorite is Dave Ramsey). I see (here in EU) that young people have 1-2 credit cards. I understand that in the US the number is higher. The dream for any young (female) professional at the tender age of 25 is to own a couple of very expensive bags ("because I deserve it" using credit cards of course).

Consumerism going steady. At least in the US you have the 401k. When I begin a discussion with friends/ acquaintances on "hey guys anyone got a decent EFT? I go my VOOG and SOXX all set up but I am looking to diversify further with some water, consumer, international, etc" and they look at me as if I speak some ancient language.

So.. most save minimal, invest nothing. Paycheck-to-paycheck is a big thing in the US and it is happening in the EU now.

(and don't get me started on parents of 14yo kids buying their kids the new iPhone every darn year)

> (and don't get me started on parents of 14yo kids buying their kids the new iPhone every darn year)

Yes, you should not get started because according to Apple’s 10-K, it does not happen on any meaningful scale. Objectively, phones are being used for longer and longer time periods.

Considering China and middle east largely dumping USD transactions and debts, you will see whatever pricing you have today to double in coming 10 years (assuming Joe and very similar to Joe quality controlling America government for coming decade - mostly now fraud so elections result wont change much). Park your money away from USD (e.g. gold or Bruneian dollar) and prepare your kids for other things than America-centric such as learning to code, and learning Chinese. My nieces are even learning Russians and Koreans beside Chinese and they are in their 20s.

Not nearly as much as inflation. Groceries alone are up something like 40% in the last 2-3 years. Your and everyone else's wages have not risen that fast on the whole.

People that were making near minimum wage before absolutely have though, and I think that's been a huge driver of the inflation. Pre-pandemic, the Walmart in our area had a starting wage of $10 or $11 an hour. It's now $18.

Can you verify the position, hours, benefits, and expectations of those offers?

'Cause I can offer (up to!) $18.50 and then negotiate down. I can also give somebody 10 hours a week and duly provide no benefits. When I worked there they took me on PT no benies, and only after proving myself did they extend an offer for FT employment. PT can be highly flexible as to the definition. Whether it's a permanent or temporary position is also something noteworthy. I think these are just some of the elements we should be considering if we're going to say wages have risen.

I can. I do high school senior photography and I asked the kids last year where they worked, and how much they made doing it. Oddly, that doesn't seem rude to ask 17 year olds.

The ones working at Walmart absolutely made $17 an hour (then). It's Walmart. They aren't playing games with stuff like that. I'm sure they're mostly doing under 32 hours a week where possible with their employees as usual.

I think a big problem, especially with companies, is that as soon as any cost of some input touches a new price level, that price now starts to get baked into the planning. Even if it was only for a very short blip, and even if the actual average costs later go down. It gets very sticky, but only in the up direction.

Have you talked to any kind of building work contractor, insurance company, etc. lately? They've all jacked up their prices just because their supply prices touched a certain level and now they have to plan for it. And to be sure, some of them are using the cover of inflation to test how willing people are to pay more.

Inflation really is a vicious cycle. And I don't think we've in recent memory seen prices actually decrease after an inflationary cycle. Do things pegged with CPI even allow for negative inflation?

This is accurate. Once the unit price is calculated with the temporarily higher input price, they are not going to reduce the unit price for as long as possible, even if input prices go down.

And what's worse? The FED does not want negative CPI. They want slowly rising CPI. A negative CPI is deflation, something they want to absolutely avoid. They don't want prices to go down. They only want them to rise up slower.

Which leads to us humans always stuck on the hedonic treadmill. If one is relying on wages, one is absolutely fcuked in this system. The only way to keep up is to keep switching jobs to a higher pay.

It’s a pretty easy problem to solve, just have wages increase automatically on an annual basis in line with changes to the CPI. That would be in addition to any raises due to good job performance or a promotion. Or even on a monthly basis during periods of high inflation. Obviously, companies avoid this simple solution because they make money on the delay between raising the price of the product they sell and when they actually start raising their worker salaries. Ideally, they want you to keep your head down and never ask for a raise.

I think just about everywhere I've worked has a cost of living raise, even entry level at restaurants. In any case this is somewhat of a contraindication to the economic planning undertaken by the Federal Reserve and their aims with inflation, which is to increase the monetary base to allow expansion. What you're proposing would, I believe in theory, close that gap as it costs employers more without necessarily increasing revenue whereas, with the current modality, things remain closer to baseline.

However, if instead of diffusing the cash through the government, it was directly granted to citizens by the government/FR one might would presume similar results as the current modality, just more beneficial to the individual. However this takes on some degree of complication: there are manifold ways to disburse it, for instance we could make a straight cut for every individual, weigh it based on income, weigh it based on wealth, and one could justify weighing in either direction - presumably the wealthy are better arbiters of economy than are the needy... But also the needy are needy and it may help alleviate some degree of disparity.

Also, inflation is difficult to measure. The CPI is not a great mark. Expanding the monetary base by 2% on paper may not result in a 2% increase in CPI. CPI is, I reckon, used as a check on the dollar's relative value, which can change dynamically as a result of cultural, economic, and political shifts on top of monetary policy. So resultsay vary, but considering market behavior over the pandemic, I think it points to a rapid dissemination of whatever money is given. I think that would probably, actually be a really efficient means to deal with inflation, however a lot of that money is actually doled out in subsidies, grants, et cetera. So a new system of public goods funding would necessarily have to be set up.

I'm glad you just solved all of our country's problems by declaring that raising workers' wages is the solution to everything. I'm sure that's got no downsides to it, huh? Why didn't we think of that before?

The problem, as stated by the comment I was responding to, was workers' wages constantly falling behind the rising cost of living and that was the solution I proposed. The commenter I was responding to proposed an alternate solution where someone is constantly switching jobs. In theory, that would work too, but obviously not feasible in practice. Where do I say I am solving "all of our country's problems"?

What I don't understand is this 2% price target. Prices could go up 10% one year, and well call it a success if next year we "tame inflation" by only having our prices go up 2%. Why can't we target to get prices back down? For those on a fixed income, this is money we lost forever. We expect (and see) some prices go down every year (mainly electronics) and it works fine. But god forbid the price of milk goes down a bit after rising 20% in two years.

Governments are afraid of deflation (prices going down) because consumers can go into a holding pattern (stopping spending while waiting for prices to continue to decrease) which can cause the economy to stall out.

Is there any evidence that modest deflation actually causes this "holding pattern" in the overall economy? I see this theory stated a lot for the reason that deflation is bad, and it definitely checks out on a basic logical level. But economics is complex right? So I'm curious what the evidence is in the real world.

I can imagine this happening with large deflation (10%, say), but what about 2% or 1%? It's not obvious to me that people would not buy a TV they really wanted if they knew it would be $392 instead of $400 next year. If consumers actually acted this sensitively toward a drop in prices, then wouldn't nearly all consumers wait for sales for all purchases? But we know that is not the case. Hell, if consumers were this sensitive toward their finances, they certainly wouldn't pay lots of interest on avoidable credit card debt, right?

It's more the bigger investments that drive a lot of the economy that are the concern - think real estate and stocks. Why buy a $1 million home today if you'll be able to buy it from $980k next year, and maybe $965k the year after that? More importantly, why continue paying the mortgage on your million dollar home when it's likely never to be worth a million again? Why buy 10,000 shares of a company now, when in a few years you could buy 10,500 shares for the same price?

That's fair - but that is assuming indefinite long-term deflation. What about intermittent modest deflation as a tool to bring prices down? It seems that just the idea of deflation is immediately rejected in any conversation about monetary policy.

Also, I think in the real world today, a home would still sell in a deflationary environment, given serious supply shortages. Especially for those buyers which are looking for a home and not an investment (investors would lose long term in a deflationary environment, as you say). Couldn't temporary, modest deflation actually open the housing market up for those "real" buyers primarily looking for a place to live?

The fear with trying for temporary deflation is it will become an out of control feedback loop, because there aren't as many "reasonable" monetary tools to combat it as there are with inflation.

Broadly it was a time of sustained growth in both the United States and United Kingdom, despite the deflation which was driven by industrialization and productivity gains. However, certain industries did suffer as a result of the deflation, so it was neither an unvarnished good or bad economic period.

As an extreme example, everyone knows about Germany hyperinflation in the 20s. Fewer people are aware that 1929-1932 was a period of massive deflation in Germany that led to the German economy collapsing, the Nazis siezing power, and 10 years later most of Europe being occupied by Fascists.

So it's pretty reasonable to be concerned about deflation.

Context matters. Prices dropped because people had less money. They didn’t drop because people were sitting on piles of cash hoping for cheaper prices next year.

It’s not silly. If you know prices are only going down you might hold off on buying that house or car until later because you know you’ll just get it cheaper.

Depends if you need a house or not, the idea that people are treating future consumption as an investment does not seem to hold much weight. In a competitive market others will be making a similar gamble meaning rents will be higher than normal due to increased demand, and the market will normalize.

Well personally I'm cutting out as much consumption as possible, how is inflation not resulting in big drops in people spending?

You know what causes a downward spiral? People stop buying things, sales drops, layoffs / cuts, people buy less, etc.

I see companies freak out over 1-2% drops in sales, how is inflation not causing people to drop consumption by 10%? I don't travel, I'm eating out WAY less, I am price/bargain hunting far more. I never buy gas without gas price map checking. I'm holding back on as much purchases as possible. I don't even think about buying any clothes not on sale. Hell, I basically don't buy clothes unless absolutely needed.

Speculative asset bubbles seem to tank money velocity more than small amounts of deflation. I think the 2% inflation target roughy yields the maximum long term sustainable capital gains tax.

If our government was actually as "green" as they say they are, they'd aim for this because consumers would slow down consumption to only buy what they need. But they know that inflation is another form of tax, and they're too greedy to say that inflation is anything but "good".

For a government, "green" isn't an end-goal, but a nice-to-have. People like the environment, but continued existence comes first, and that in turn required having a huge economy in order to make a huge military affordable, and that military is needed to maintain the continued existence of the government (as an institution rather than the specific jobs of specific people within it).

Stickiness of nominal wages means thaf deflation leads to more rapid downsizing in industries facing slowdowns (including transitoy ones), which is among the reasons that the Fed, faced with a dual mandate of price stability and promoting full employment, prefers small positive inflation. There's also reason to believe that deflation is more likely to be sticky once entrenched than inflation, because the knock-on effects produce more deflation.

> For those on a fixed income, this is money we lost forever.

Yes, that's a fundamental problem with fixed incomes and why minimum support programs don't tend to use fixed nominal benefits across time. Most people aren’t on fixed incomes, and if we tried to manage price levels around people on fixed incomes, not only would it be bad for everyone else, but it would also threaten the investments underlying the sources of those fixed incomes (which aren’t really fixed, because they can drop, including to 0.)

Deflation means a dollar tomorrow is always worth more than a dollar today meaning a rational person should strive to spend as little money today as possible. This eventually locks the entire economy up into a death spiral.

I'm curious to know if this is a real phenomenon that has been observed. Would you be able to point me in the direction of resources to learn more about this?

The reason for my skepticism is that even without deflation, a dollar tomorrow is usually worth more than a dollar today, yet tons of people* don't save or invest much/any of their money, even if they're able to.

* I'm speaking from the perspective of an American FWIW.

And they will simply take your physical dollar and store it deeeep under the ground where no wild west thieves can steal it or even look at it, so that they can store it until tomorrow where it will be worth more!

The US economy was absolutely fucked for a large portion of that time period largely because of the lack of monetary policy. The economy has done much, much better since we introduced fiat.

Milton Friedman in "Monetary History of the United States" shows that fluctuations in the money supply were significantly more pronounced after fiat money began. The fed's enlightened hand on the tiller simply isn't as good as the blind actions of the free market.

Even with the prices of commodities falling, stock prices can still rise, and as long as this is higher than the deflationary rate, investing still beats hoarding.

Between 2008 and 2018 milk prices went down from $3.80 a gallon to $2.90 [1]. So we're actually barely above 2008 prices in non-inflation adjusted dollars.

To your specific point about targeting negative inflation, that's deflation, which most people believe is bad for the economy. Even if there are types of "good deflation", government policy inentionally targeting deflation would almost definitely be a bad thing.

Most of the other responses are missing the point of your question. You really asking why central banks don't engage in targeting the price level, rather than price changes (=inflation). In price level targeting, they'd aim for higher (lower) inflation next year if they under-(over-)shot their target this year.

Academics and have studies the pros and cons. I don't have time to post summaries, but maybe someone else can step in:

It’s because that’s called deflation and mainstream economics predicts that it is absolutely catastrophic to the economy, at least if it is seen generally across the whole economy. Obviously, individual goods can decrease in nominal price, but general deflation is thought to lead almost immediately to depressions and recessions.

>> What I don't understand is this 2% price target.

It is statistical trickery and a headline number used to make people think things are OK. It is also a convenient number for COLA increase targets which make people think their incomes/pensions are going up (when effectively they are not on a real basis.)

Also, as you note, we re-baseline each year and dont talk about the cumulative compounded inflation e.g., over the past 5yrs.

Americans on fixed incomes (e.g., pension, social security) and those without wage elasticity (e.g., restaurant workers) are absolutely miserable right now because they are squeezed from both sides, even after modest wage increases in 2021/2022. This is not good for a Democracy.

>> Low wage workers have actually seen the most wage growth recently.

Yes and no(?)

From the study "Real wage growth across the wage distribution, 2019–2022" shows 9% real wage growth. The "real" portion is compared to engineered inflation figures. In the day-to-day world where people pay actual prices, price increases have not be 2% or whatever CPI claims them to be, they are much worse.

We can back into rosy numbers, but the real numbers are felt by people. I'd suggest speaking to a variety of people and see how they feel. Ensure to also speak to someone on social security income. I speak to my mom and see the numbers on a weekly basis.

I didn't say anything about the wage price spiral. One category that has had above-average inflation is food away from home. That's mostly driven by wages of the workers, not wages of the clientele.

The pesky law you mention is indeed the issue. Not enough people are willing to work in restaurants, and/or not enough people are willing to modify their habits to avoid eating in restaurants when the prices increase.

Whether "printing" money was a cause of generalized inflation is a matter of debate. It's hard to argue it didn't have some effect, but I think you'd probably expect the inflation to have been worse if it were just dependent on the amount of dollars in the system. Given the tightness in the labor market and reduced workforce participation, it seems to me that the pandemic was a large-scale, impromptu test of the UBI, and society failed it very badly. Turns out people will actually not work if they don't have to, and robots are not yet prepared to pick up the slack.

> Whether "printing" money was a cause of generalized inflation is a matter of debate.

It's only a debate for people who haven't looked at the history of money and inflation. Inflation is always the result of an increase in the supply of money relative to the value of goods and services in the economy. It happens when there are gold rushes, silver rushes, and running the government printing press.

Our current inflation happened soon after a massive increase in deficit spending.

You’re supposed to be getting raises to keep up with inflation. Inflation means rising cost of everything, including your labor. What is your source of a fixed income? Even social security has cost of living adjustments.

If it’s an annuity, you can get annuities that vary based on changes to the CPI. If you put a lot of money into a fixed annuity years ago, you did not properly hedge interest rate/inflation risk.

Some inflation is seen as good by economists because it pushes money that would sit on the sidelines into "productive" uses. It creates an incentive and a need for risk taking or stored wealth will be eaten away. That this doesn't align with most individual's goal is of no concern to those most interested in productivity and GDP growth.

> Some inflation is seen as good by economists because it pushes money that would sit on the sidelines into "productive" uses.

The ever-popular Scrooge McDuck cash vault theory. Nobody has a cash vault. Any "cash" is stored in banks, which loan it out into the economy. People who borrow money save/spend it.

People get hired off the 2% because that’s a baseline level of growth. When the economy is in deflation people will constantly get fired every year, growth basically stops, and you end up with a highly risk averse Japan-type situation.

This is a drastic oversimplification but that’s basically it

I feel blessed to work in Tech, where -- however bad the economy is -- most of us dont face absolute deprivation as those in some other industries.

That said, basic expectations of things growing up are just unreachable for many. My parents lived much more comfortable lives than I do. My grandparents even more so.

US leaders should be careful. People get upset when they have nothing to feed their children. I hope we solve these problems with sensible fiscal and monetary policy.

My parents lived much more comfortable lives... grandparents even more so...

Interesting how you stopped at "grandparents".

To be clear, absolutely not intended as any kind of attack on you or what you've written - just some thoughts passed on to me that made it easier to be grateful for that which is in my life, period:

Consider past generations - we're in "the 1%" by that metric alone. No / hardly (any "real") medicine, completely unstable food supplies, other tribes coming over the hills and killing everyone ... and, that's describing more of the "history" part of human existence, to date.* Further, a core bias of psychology is "the golden age bias".** Including feelings as simple as: when events are in the past, things can seem so "neat", "orderly", and ... "simple". Oh for one income to feed a family of four, right? But, how many had that experience - what proportion? And, that ties in with "survivor bias" etc.

Don't get me wrong, instability is a PITA. I get where you're coming from. It's not as though I don't have such thoughts. But, I can always come back to various bits of wisdom I've picked up from a myriad of sources, including a phrasing I've always liked that AFAIK is from Bill Maher:

If you think you have it tough, read history books.

That always helps me to remember that I didn't just watch my village burn to the ground due to the Mongol or European or etc. raiders, my relatives get raped and murdered, my child die of ... well, just about anything ...

... maybe some in this thread will find these ideas useful as well.

* Zooming out a bit more ... I always find it amusing walking in a park, especially - hearing the birds chirping, seeing the squirrels "frolicking" ... what passes for a pleasant "pastoral" experience for us, is filled with advertisements for sex / nasty "neighbor property line disputes" (birds chirping), animals desperately trying to find the next meal or water, etc.

Also just the proportion of people doing HARD jobs. Being a farmer was brutal and not long ago 70% of the population worked in agriculture; now it’s like 2%. Machinery had simplified many tasks from ag labor to even housework. The laundry machine has been a game changer for women I’ve heard.

1000% agree with you that things were much worse once we go beyond grandparents. Just antibiotics and democracy alone have improved every person's life.

>> AFAIK is from Bill Maher: If you think you have it tough, read history books.

Be careful when Conservatives tell you to be complacent or grateful. There is a typical line "you are worrying about your $15hr minimum wage when kids half your age work in coal mines".

You can use such arguments for all sorts of nefarious purposes "you think your public school is overcrowded? go to Africa" "you think healthcare in the US is bad? go to rural Nepal" "you think crime is high in SF? go to 1800s NYC"

But why should we aspire to that? Why not aspire to more?

> That said, basic expectations of things growing up are just unreachable for many. My parents lived much more comfortable lives than I do. My grandparents even more so.

My wife’s grandma got married as a teenager to a trucker passing by because her family couldn’t support all their kids. This was not unusual in that generation.

Firstly I'm sorry to hear about your family's situation. I certainly dont mean to imply everything was rosy.

I will compare very roughly and anecdotally across generations. I'm an Engineer (CS). So was my father, though he ended up doing accounting. So was my grandfather (civil.)

My grandfather owned a home by 23 on his engineering salary.

My father owned a comfortable home by 35 on his salary. The salary:homeprice ratio was almost 1.5:1

My salary:homeprice ratio for the same exact house as my father is 4:1. Arguably, i'm better educated than my father and grandfather, and have much better credentials.

Im not trying to be ungrateful for what has been given to me, but the ratios seem completely off.